The SEC Just Dropped the Tokenization Playbook

(And It’s Not the “Crypto Loophole” Some People Wanted)

Tokenization has officially graduated from “cool demo” to “adult supervision.”

On January 28, 2026, SEC staff across Corp Fin, Investment Management, and Trading & Markets published a joint Statement on Tokenized Securities that does one thing extremely well: it kills ambiguity.

Here’s the money line, translated into plain English:

If it’s a security, it’s a security. Putting it on a blockchain does not magically turn it into something else. The blockchain is just the new record-keeping format, not a new legal category.

And I’m going to say the quiet part out loud: this is bullish for real tokenization (especially real estate), because institutions don’t invest in “hope.” They invest in enforceable rights, clean records, and regulated rails.

What the SEC Actually Said (No Hype, Just Mechanics)

The SEC staff defines a “tokenized security” as a traditional security (as defined under federal securities laws) that’s formatted as or represented by a crypto asset, where the ownership record is maintained in whole or in part on a crypto network.

Then they split the world into two big buckets:

1) Issuer-sponsored tokenized securities (the “real deal” model)

This is where the issuer (or its agent) uses DLT as part of the master securityholder file so that a token transfer maps to a change in the official ownership record.

They also acknowledge a variation where the issuer’s “master file” is offchain, and the onchain token is used to trigger updates to the official record.

My take: this is the serious lane. If you want “tokenized shares” that stand up in court, in audits, and in M&A, you build here.

2) Third-party tokenized securities (the “be careful” model)

This is where someone not affiliated with the issuer tokenizes an underlying security.

SEC staff highlights two common patterns:

Security entitlement model: the third party creates a crypto-asset representation of a security entitlement (think indirect ownership plumbing).

Linked / synthetic model: the third party issues a “linked security” giving synthetic exposure to a referenced security, without conveying rights from the referenced issuer.

And they go further: some synthetic structures may walk and quack like a security-based swap, depending on economics and the “swap” definition/exclusions.

My take: this is where people get cute and then get crushed. The SEC explicitly flags extra risk for holders here, including exposure to the third party’s bankruptcy risk.

The Real Message: “Same Rules, Smarter Rails”

The staff statement is also very clear about scope: it’s a staff view (not a rule), and it doesn’t change existing law.

But as a practical matter, it’s a roadmap for anyone trying to build tokenized issuance without stepping on legal landmines:

Registration or exemption still applies (Securities Act is not optional just because the asset is onchain).

Rights matter: if tokenized and traditional versions have substantially similar rights, the SEC staff suggests they may be treated as the same class for certain purposes.

Recordkeeping is king: the master securityholder file (onchain, offchain, or hybrid) is the anchor.

Economic reality wins over labels (especially when you drift into “linked” or swap-like territory).

My opinion: tokenization is no longer a compliance question. It’s a systems architecture question. The winners will be the teams that can engineer “regulated truth” across issuance, transfer, custody, and trading without breaking the user experience.

What This Means for Real Estate Tokenization (The Lane Is Clearer Now)

Real estate tokenization is best positioned when it’s honest about what it is:

An ownership interest in an entity (LLC, LP, trust, REIT-like vehicle), or

A debt instrument (note, bond, revenue share), or

A fund interest.

The SEC staff statement doesn’t “approve” real estate tokenization, but it does something just as valuable: it clarifies how tokenization fits into known categories, and it separates issuer-sponsored ownership from third-party synthetic exposure.

If you’re tokenizing real estate and your pitch is “we bypass the old system,” you’re late and wrong.

The pitch is: we upgrade the rails while keeping investor protections intact.

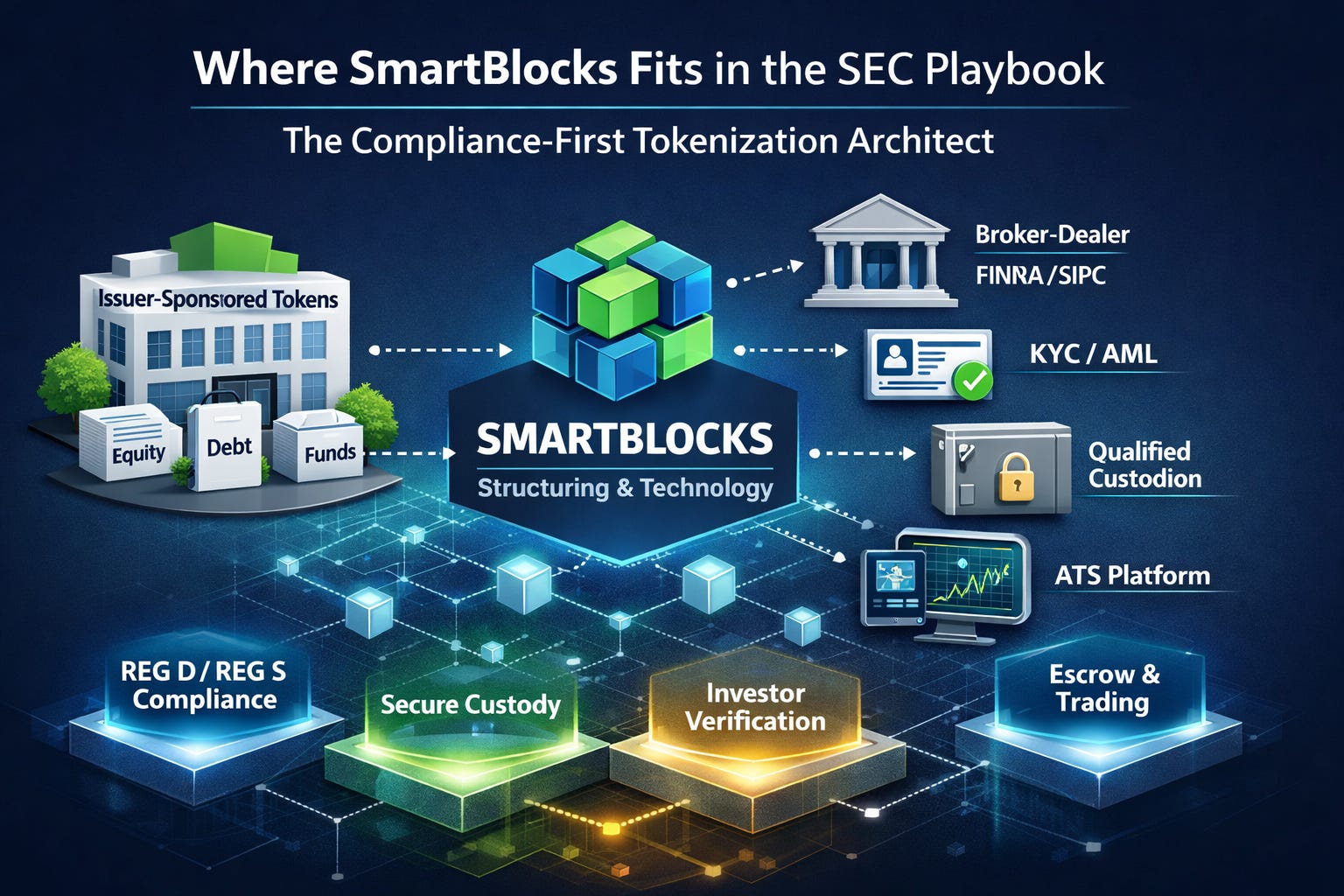

Where SmartBlocks Fits in This Playbook (Based on Public Materials)

Using the SEC’s taxonomy, SmartBlocks sits firmly in the issuer-sponsored, regulated-securities lane, not the “synthetic exposure” lane.

1) We’re the structuring + rails partner, not the broker-dealer

SmartBlocks is not a broker-dealer and we don’t pretend to be.

What we do is design and implement the tokenization structure so it can run inside the existing securities framework and we partner with registered broker-dealers, ATSs, escrow, KYC/AML providers, and qualified custodians when the transaction requires it.

Translation: we build the compliant machine; regulated partners operate the regulated functions.

2) Issuer-sponsored tokenization built around real ownership and clean records

We focus on structures where tokens represent real, legally enforceable interests (equity, debt, fund interests, SPV/LLC units) not “price-tracking tokens” or proxy economics.

And we design the system so the issuer’s ownership records are authoritative, reconcilable, and audit-ready whether the official ledger is onchain, offchain, or hybrid.

3) The compliance stack is intentional, not “bolted on later”

SmartBlocks helps clients operationalize the full stack the SEC actually cares about:

Offering exemptions / disclosures (e.g., Reg D / Reg S alignment where applicable)

Transfer restrictions + investor eligibility logic

KYC/AML + accreditation workflows via partners

Escrow flows + subscription mechanics

Custody strategy via qualified custodians when required

Trading pathway via BD/ATS partners when secondary liquidity is part of the plan

Bottom line

SmartBlocks is the compliance-first tokenization architect: we help issuers tokenize as securities, using regulated partners where the law requires it, so the end product is institutional-grade instead of “crypto-grade.”

My 3 Predictions (Because This Is Where It Gets Fun)

Prediction 1: 2026 becomes the year of “issuer-sponsored everything”

The market is going to pivot hard toward tokenization models where the token transfer is meaningfully tied to the official ownership record (onchain master file or hybrid). The “wrapped it and prayed” era gets squeezed by compliance reality.

Prediction 2: Synthetic tokenized equities will get regulated like a hornet’s nest

Anything that smells like a linked security or security-based swap will face higher friction, higher legal cost, and lower distribution. Many of these products will either (a) die, or (b) move upmarket to eligible participants and heavily controlled venues.

Prediction 3: The biggest winners will not be “crypto exchanges,” they’ll be the boring operators

The companies that win will look “boring” on the surface: broker-dealers, ATS operators, transfer-agent-grade recordkeeping, qualified custody, audit trails. The UX can still feel modern, but the backend will be regulated and buttoned-up. That’s how institutional capital shows up.

The Practical Takeaway

If you’re an issuer or sponsor: choose your model upfront. Are you tokenizing actual ownership, with an authoritative record? Or are you creating synthetic exposure (and inheriting derivatives complexity)?

If you’re building a platform: stop selling “tokenization.” Start selling compliance-grade rails that happen to be onchain.

If you’re an investor: demand clarity on rights (cash flows, voting, transfer restrictions, custody, and what happens in a platform bankruptcy). The SEC staff basically told you where the bodies are buried.